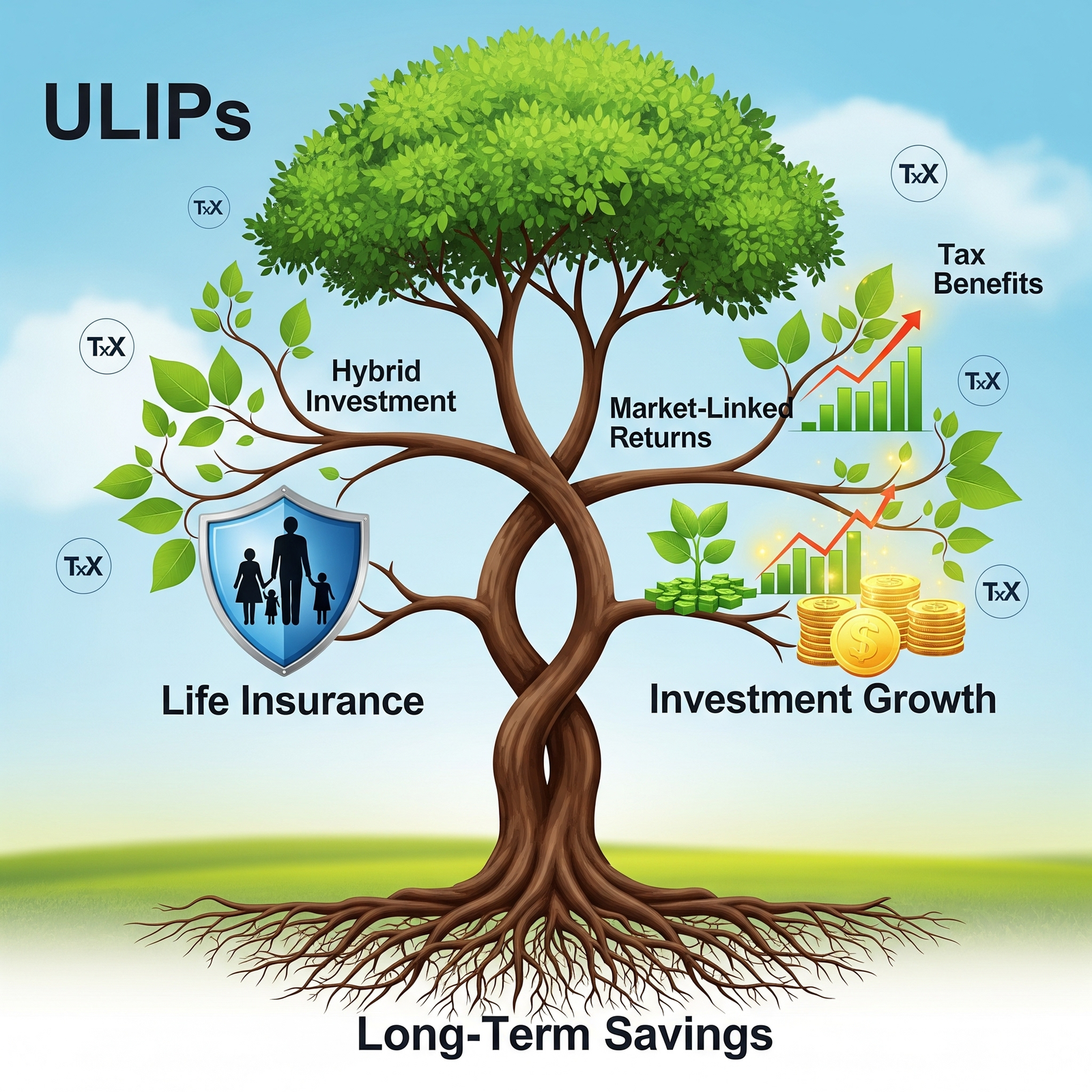

In the evolving landscape of personal finance, Unit Linked Insurance Plans (ULIPs) have carved out a distinct niche. Often misunderstood, ULIPs are not just an insurance policy or a pure investment vehicle; they are a hybrid investment product that ingeniously blends the security of life insurance with the potential for substantial investment growth. For those seeking a single solution to protect their loved ones while actively growing their wealth, ULIPs offer a unique proposition that goes beyond conventional financial products.

The Uniqueness: A Two-in-One Financial Powerhouse

The core strength of a ULIP lies in its dual benefit structure. A portion of the premium you pay goes towards providing life insurance coverage, ensuring a safety net for your family in your absence. The remaining, larger portion is invested in various market-linked funds of your choice, allowing you to participate directly in the market’s upside. This insurance-cum-investment approach provides both financial protection and wealth creation opportunities under one umbrella.

Navigating the Investment Landscape: Your Choice, Your Control

What truly makes ULIPs dynamic is the control they offer over your investment strategy. Policyholders can choose from a range of fund options, typically including:

- Equity Funds: For those with a higher risk appetite seeking aggressive investment growth.

- Debt Funds: For conservative investors looking for stable returns and capital preservation.

- Hybrid/Balanced Funds: Offering a mix of equity and debt for a moderate risk-return profile.

A key feature is the ability to perform fund switching. As your risk appetite changes, market conditions shift, or your financial goals evolve, you can seamlessly move your accumulated units from one fund to another without incurring tax liabilities. This professional fund management by the insurer, combined with your ability to adapt, makes ULIPs highly responsive to personal and market dynamics.

Flexibility Redefined: Adapting to Life’s Rhythms

Modern ULIPs are designed with remarkable flexibility, acknowledging that life’s financial needs are rarely static:

- Partial Withdrawals: After a mandatory lock-in period (typically five years), you can make partial withdrawals from your fund value to meet unforeseen expenses or planned milestones like a child’s education or a down payment for a home. This offers valuable liquidity without surrendering the entire policy.

- Premium Holidays: Some ULIPs offer the option to take a “premium holiday,” allowing you to temporarily stop paying premiums during periods of financial strain, while your policy continues based on the accumulated fund value.

- Top-Up Premiums: You can also invest additional lump sums as “top-up premiums” to capitalize on favorable market conditions or to boost your long-term corpus.

Tax Benefits: A Double Advantage

ULIPs come with compelling tax benefits, making them an attractive proposition for long-term savings and financial planning:

- Premiums paid are eligible for tax deductions under Section 80C of the Income Tax Act.

- The maturity proceeds or the death benefit received are typically exempt from income tax under Section 10(10D), subject to certain conditions.

This dual tax advantage on both investment and maturity makes ULIPs a tax-efficient route to wealth creation.

The Evolution: Transparency and Long-Term Value

In their early days, ULIPs sometimes faced criticism for high charges and complexity. However, significant regulatory reforms have transformed them into more transparent and investor-friendly products. Charges are now capped, and disclosures are clearer, ensuring that a larger portion of your premium is invested.

The true potential of ULIPs is realized over the long-term investment horizon. By staying invested through market cycles, the power of compounding combined with strategic fund switching can lead to substantial market-linked returns, helping you achieve significant financial milestones.

In essence, ULIPs are an ideal instrument for individuals who seek the dual comfort of securing their family’s future and participating in market growth through a disciplined, flexible, and tax-efficient approach. They are not merely policies; they are a sophisticated financial tool designed for the modern investor charting a course towards long-term financial freedom.